Chapter 5 - Estimates, Confidence Intervals, and Hypothesis Tests

In this chapter, we discuss the fitting criterion that NONMEM uses, parameter estimates, and standard error estimates. We then discuss how to form confidence intervals for parameters and do hypothesis tests with NONMEM.

In principle, all fitting procedures attempt to adjust the values of the parameters of the model to give a "best fit" of the predictions to the actual observations. The set of parameters that accomplish this are called the parameter estimates, and are denoted here as

,

, and

, and

. Methods differ in how they define "best". The

criterion that NONMEM uses is a Least Squares (LS) type

criterion. The form of this criterion varies as the error

model varies, and as population models with multiple random

effects must be considered. We briefly discuss these various

criteria next, to give the reader a feel for what NONMEM is

doing. A detailed knowledge of the statistical basis for the

choice of fitting criterion is not necessary either to use

or interpret NONMEM fits. In this chapter, a fixed effects

parameter will be denoted by a

. Methods differ in how they define "best". The

criterion that NONMEM uses is a Least Squares (LS) type

criterion. The form of this criterion varies as the error

model varies, and as population models with multiple random

effects must be considered. We briefly discuss these various

criteria next, to give the reader a feel for what NONMEM is

doing. A detailed knowledge of the statistical basis for the

choice of fitting criterion is not necessary either to use

or interpret NONMEM fits. In this chapter, a fixed effects

parameter will be denoted by a

; the distinction between individual fixed effects

parameters (

; the distinction between individual fixed effects

parameters (

) and population fixed effects parameters will not be

important here.

) and population fixed effects parameters will not be

important here.

For the Additive error

model (3.4), the Ordinary Least Squares criterion (OLS)

chooses the estimate

so as to make the sum of squared (estimated) errors as small

as possible. These estimates cause the prediction, here

denoted

so as to make the sum of squared (estimated) errors as small

as possible. These estimates cause the prediction, here

denoted

, to be an estimate of the mean value of

, to be an estimate of the mean value of

, which is intuitively appealing. The prediction is obtained

by computing the value for y under the model with parameters

set to their estimated values and

, which is intuitively appealing. The prediction is obtained

by computing the value for y under the model with parameters

set to their estimated values and

set to zero†.

set to zero†.

----------

†

, not

, not

, since we follow the NONMEM convention and, when discussing

individual type data as here, use

, since we follow the NONMEM convention and, when discussing

individual type data as here, use

to denote the random effects of a single level that appear

in the model, those in the residual error model.

to denote the random effects of a single level that appear

in the model, those in the residual error model.

----------

The simple OLS criterion

just defined becomes inefficient and is no longer the

"best" one to use when the error model is other

than the Additive error model. It treats all estimated

errors as equally important (i.e. a reduction in the

magnitude of either of two estimated errors that are of the

same magnitude is equally valuable in that either reduction

decreases the sum of squared errors by the same amount), and

this results in parameter estimates that cause all errors to

have about the same typical magnitude, as assumed under the

Additive model. The CCV error model, though, says that the

typical magnitude of an error varies monotonically with the

magnitude of the (true) prediction of y. In principle,

Weighted Least Squares (WLS) gives a fit more commensurate

with the CCV or other non-Additive error model. WLS chooses

as that value of

as that value of

minimizing

minimizing

Each

is a weight which, ideally, is set proportional to the

inverse of the variance of

is a weight which, ideally, is set proportional to the

inverse of the variance of

. In the CCV model this variance is proportional to

. In the CCV model this variance is proportional to

(evaluated at the true value of

(evaluated at the true value of

). Use of such weights will down-weight the importance of

estimated squared errors associated with large values of

). Use of such weights will down-weight the importance of

estimated squared errors associated with large values of

and promote the relative contribution of those associated

with small values of

and promote the relative contribution of those associated

with small values of

.

.

In many cases, users can

supply approximate weights, and the WLS objective function

can be used as stated in (5.1). When, as with the CCV model

for example, the ideal weights depend on the true values of

parameters, these true values can be replaced by initial

estimates, and then the WLS objective function as given in

(5.1) can be minimized. Alternatively, instead of viewing

as a function of

as a function of

only through the estimated error’s dependence on

only through the estimated error’s dependence on

, it can be viewed as a function of

, it can be viewed as a function of

through both that dependence and also through the

ideal weights’ dependence on

through both that dependence and also through the

ideal weights’ dependence on

. The entire function can then be minimized with respect to

. The entire function can then be minimized with respect to

. That this creates a problem is most easily seen when the

error model contains a parameter which is not itself a

parameter of the structural model, but which, nonetheless,

must be regarded as an element of

. That this creates a problem is most easily seen when the

error model contains a parameter which is not itself a

parameter of the structural model, but which, nonetheless,

must be regarded as an element of

. Such an error model is the Power Function model of (3.7),

and the "extra" parameter is

. Such an error model is the Power Function model of (3.7),

and the "extra" parameter is

. The WLS objective function with the reciprocal variance of

. The WLS objective function with the reciprocal variance of

substituted for

substituted for

is†

is†

----------

† Again, we

call attention to the symbols used for the random effects

parameter: the term

appears in the objective function, (5.2), not

appears in the objective function, (5.2), not

, because we are discussing individual type data, not

population type data.

, because we are discussing individual type data, not

population type data.

----------

In this case if

were set to a very large number, while the other parameters

in

were set to a very large number, while the other parameters

in

were only such as to make all

were only such as to make all

, then all

, then all

would be very large, and the summation would attain a very

small value. (The value of

would be very large, and the summation would attain a very

small value. (The value of

is irrelevant to the minimization with respect to

is irrelevant to the minimization with respect to

.) Thus, all elements in

.) Thus, all elements in

other than

other than

would be indeterminate (as long as they were such that all

would be indeterminate (as long as they were such that all

were greater than 1); a most unsatisfactory state of

affairs.

were greater than 1); a most unsatisfactory state of

affairs.

There is a way to deal

with this problem that preserves the spirit of least-squares

fitting, and NONMEM uses it. In essence, it adds to the WLS

objective function a term proportional to the sum of the

logarithms of the error variances. Thus a penalty is paid

for increasing the error variances without a concomitant

decrease in the estimated errors themselves. This modified

objective function is called the Extended Least Squares

(ELS) objective function. It is minimized with respect to

all parameters of the structural and error models

simultaneously (in the current example,

and

and

, as

, as

can be considered an element of

can be considered an element of

). Note that the objective function may be negative. This

has no particular significance.

). Note that the objective function may be negative. This

has no particular significance.

The complications arising

from a population model are due entirely to the random

interindividual effects occurring in the parameter model. To

deal with this, NONMEM uses an approximation to the true

model. The approximate model is linear in all the random

effects. For this linearized model, the vector of mean

values for the observations from the

individual is the vector of true predictions for these

observations. These predictions are obtained from the model

by setting the parameters to their true values and by

setting all the elements of both

individual is the vector of true predictions for these

observations. These predictions are obtained from the model

by setting the parameters to their true values and by

setting all the elements of both

and

and

to zero. In other words, these are the true predictions for

the mean individual with fixed effects equal to those of the

to zero. In other words, these are the true predictions for

the mean individual with fixed effects equal to those of the

individual. For this linearized model it is also possible to

write a formula for the variance-covariance matrix of the

observations from the

individual. For this linearized model it is also possible to

write a formula for the variance-covariance matrix of the

observations from the

individual. This matrix is a function of the

individual’s fixed effects and the population

parameters

individual. This matrix is a function of the

individual’s fixed effects and the population

parameters

,

,

, and

, and

. Finally, the ELS objective function discussed above is

generalized to be a sum over individuals, rather than

observations, and where the

. Finally, the ELS objective function discussed above is

generalized to be a sum over individuals, rather than

observations, and where the

term of the sum involves a squared error between a vector of

observations and an associated vector of predictions,

weighted by the reciprocal of the associated

variance-covariance matrix for the

term of the sum involves a squared error between a vector of

observations and an associated vector of predictions,

weighted by the reciprocal of the associated

variance-covariance matrix for the

individual.

individual.

It is useful to consider

how to estimate parameters that do not appear in the model

we use to fit the data, but are, instead, functions of them

(e.g. the half-life parameter

, when the rate constant of elimination

, when the rate constant of elimination

is the model parameter).

is the model parameter).

It is always possible, of

course, to parameterize the model in the function of

interest. For example, we have already seen (Chapters 2

& 3) that we may use the function (parameter)

in the one-compartment model instead of

in the one-compartment model instead of

. However, we may be interested in the values of several

alternative parameterizations (e.g., we may want to know k,

clearance, and half-life). Rather than rerun the same

problem with several alternative parameterizations, we can

use the fact that the LS estimate of a function of the

parameters is given by the same function of the LS parameter

estimates. Formally, if

. However, we may be interested in the values of several

alternative parameterizations (e.g., we may want to know k,

clearance, and half-life). Rather than rerun the same

problem with several alternative parameterizations, we can

use the fact that the LS estimate of a function of the

parameters is given by the same function of the LS parameter

estimates. Formally, if

is the function of interest, then

is the function of interest, then

. E.g. Letting

. E.g. Letting

,

,

, and

, and

, then

, then

.

.

Clearly, it is almost

impossible for the estimates to actually be the true values.

The question is: how far are the true values from the

estimates? To discuss this question, imagine replicating the

entire experiment (gathering new data, but keeping

fixed) multiple times. Also, for simplicity, imagine that

the model has only one scalar parameter,

fixed) multiple times. Also, for simplicity, imagine that

the model has only one scalar parameter,

, and that its true value,

, and that its true value,

is known. If, after each replication, the estimate of

is known. If, after each replication, the estimate of

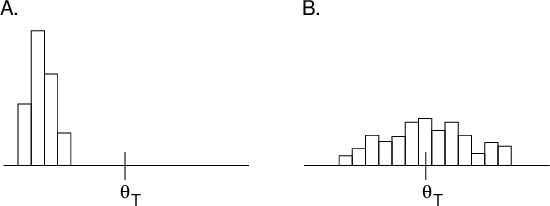

is recorded, and a histogram of these values is plotted, one

might see something like figure 5.1A or 5.1B.

is recorded, and a histogram of these values is plotted, one

might see something like figure 5.1A or 5.1B.

Figure 5.1. Two

hypothetical histograms of estimates of a single parameter

upon replication of a given experiment. Left panel (A): The

estimates have small variance (spread) but are biased (the

mean of the estimates differs from the true value,

); Right panel: The estimates have large variance but are

relatively unbiased.

); Right panel: The estimates have large variance but are

relatively unbiased.

The difference between

the estimate and the true value,

, obviously differs from replication to replication. Let

this difference be called the estimation error. We

cannot know the estimation error of any particular estimate

(if we could, we could know the true value itself, by

subtraction), but we can hope to estimate the mean error

magnitude. Since errors can be positive or negative, a

measure of magnitude that is unaffected by sign is

desirable. This is traditionally the Mean Squared Error (

, obviously differs from replication to replication. Let

this difference be called the estimation error. We

cannot know the estimation error of any particular estimate

(if we could, we could know the true value itself, by

subtraction), but we can hope to estimate the mean error

magnitude. Since errors can be positive or negative, a

measure of magnitude that is unaffected by sign is

desirable. This is traditionally the Mean Squared Error (

). The MSE can be factored into two parts:

). The MSE can be factored into two parts:

where

is the bias of the estimates (mean (signed) difference

between the estimates and the true value) and

is the bias of the estimates (mean (signed) difference

between the estimates and the true value) and

is the standard error of the estimates (

is the standard error of the estimates (

is the variance of the estimates). As illustrated in figure

5.1, the

is the variance of the estimates). As illustrated in figure

5.1, the

can be about the same for two types of estimates while both

their bias and

can be about the same for two types of estimates while both

their bias and

differ. It is very hard to estimate the bias of an estimator

unless the true parameter value is, in fact, known. This is

not true of the

differ. It is very hard to estimate the bias of an estimator

unless the true parameter value is, in fact, known. This is

not true of the

: the standard deviation of the distribution of estimates of

a parameter on replication is the

: the standard deviation of the distribution of estimates of

a parameter on replication is the

; no knowledge of the true value of the parameter is

required. In many situations, LS estimators of fixed effects

parameters are unbiased, although in nonlinear problems,

such as most pharmacokinetic ones, this cannot be

assured.

; no knowledge of the true value of the parameter is

required. In many situations, LS estimators of fixed effects

parameters are unbiased, although in nonlinear problems,

such as most pharmacokinetic ones, this cannot be

assured.

Figure 5.1 illustrates

the distribution of parameter estimates that might result if

an experiment were replicated. The bias and spread depend on

the estimation method, the design of the experiment (

, which implicitly includes

, which implicitly includes

) and on the true parameter values, including the variances

(and covariances) of the random effects influencing

) and on the true parameter values, including the variances

(and covariances) of the random effects influencing

. If, for example, more observations were obtained in each

experiment (more individuals in a population study), the

spread of the estimates (one from each experiment) would

decrease until, in the limit, if an infinite number of

observations were obtained in each experiment, every

estimate would be the same (equal to the true value plus the

bias of the estimator). Thus, the distribution of the

estimate tells us nothing about biology or measurement

error, but only about the

. If, for example, more observations were obtained in each

experiment (more individuals in a population study), the

spread of the estimates (one from each experiment) would

decrease until, in the limit, if an infinite number of

observations were obtained in each experiment, every

estimate would be the same (equal to the true value plus the

bias of the estimator). Thus, the distribution of the

estimate tells us nothing about biology or measurement

error, but only about the

of the estimate itself.

of the estimate itself.

In contrast,

and

and

tell us about unexplained (or random) interindividual

variability (biology) or error magnitude (biology plus

measurement error), not about how precisely we know these

things. No matter how many observations we make,

interindividual variability will remain the same size (but

the variability of our estimate of its size will decrease),

as will the measurement error variability of a particular

instrument.

tell us about unexplained (or random) interindividual

variability (biology) or error magnitude (biology plus

measurement error), not about how precisely we know these

things. No matter how many observations we make,

interindividual variability will remain the same size (but

the variability of our estimate of its size will decrease),

as will the measurement error variability of a particular

instrument.

It is very important not

to confuse variability (e.g., between individuals) in a

model parameter with variability in the estimate of that

parameter, despite the fact that the terms we use to

describe both variabilities are similar. Thus an element of

, say

, say

has a

has a

,

,

, while the estimate of

, while the estimate of

,

,

, also has a

, also has a

given by the square of the standard error for

given by the square of the standard error for

. Indeed, the use of the term "standard error"

rather than "standard deviation" to name a measure

of the spread in the distribution of the parameter

. Indeed, the use of the term "standard error"

rather than "standard deviation" to name a measure

of the spread in the distribution of the parameter

rather than in the parameter helps call attention to the

distinction between these two types of things.

rather than in the parameter helps call attention to the

distinction between these two types of things.

Acknowledging that any particular estimate from any particular experiment is unlikely to equal the true parameter value implies that we should be interested in "interval" estimates of parameters as well as (instead of?) point estimates. An interval estimate of a parameter is usually a range of values for the parameter, often centered at the point estimate, such that the range contains the true parameter value with a specified probability. The probability chosen is often 95%, in which case the interval estimate is called the 95% Confidence Interval (CI).

A CI is often based only

on the parameter estimate and its

. In the next sections we discuss three questions about such

CIs a little further. (i) How to estimate the

. In the next sections we discuss three questions about such

CIs a little further. (i) How to estimate the

from a single set of data (we cannot replicate our

experiment many times and construct a histogram as in figure

5.1). (ii) Given an estimate of

from a single set of data (we cannot replicate our

experiment many times and construct a histogram as in figure

5.1). (ii) Given an estimate of

, how to use that number to compute a (95% confidence)

interval with 95% chance of containing the true parameter

value. (iii) Given an estimate of

, how to use that number to compute a (95% confidence)

interval with 95% chance of containing the true parameter

value. (iii) Given an estimate of

, how to compute a confidence interval for a function of the

parameter.

, how to compute a confidence interval for a function of the

parameter.

Remarkably, the

of a parameter estimate can be estimated using only the data

from a single experiment. The idea is that the data give us

estimates of the variances of all random effects in our

model, from which we can estimate the variability in future

data (if we were to replicate the experiment). That is, the

SE of the estimates on replication depends only on

quantities we either know or have estimates of: the

of a parameter estimate can be estimated using only the data

from a single experiment. The idea is that the data give us

estimates of the variances of all random effects in our

model, from which we can estimate the variability in future

data (if we were to replicate the experiment). That is, the

SE of the estimates on replication depends only on

quantities we either know or have estimates of: the

, the number of

, the number of

observed (

observed (

), and the variances of all random effects.

), and the variances of all random effects.

It is a little beyond the

scope of this discussion to give the method by which NONMEM

actually estimates the

of a parameter estimate; however, examples of how this can

be done are found in any statistical textbook on regression.

NONMEM presents the estimated standard error for each

parameter of the model (including the random effects

parameters,

of a parameter estimate; however, examples of how this can

be done are found in any statistical textbook on regression.

NONMEM presents the estimated standard error for each

parameter of the model (including the random effects

parameters,

and

and

) as part of its output.

) as part of its output.

Statistical theory tells

us not only how to compute the

of a parameter estimate, but also that for a LS estimate

(and many other kinds of estimates), the shape of the

distribution of the estimates is approximately Normal if the

data set is large enough. This means that we may use

percentiles of the Normal distribution, to compute

confidence interval bounds (when

of a parameter estimate, but also that for a LS estimate

(and many other kinds of estimates), the shape of the

distribution of the estimates is approximately Normal if the

data set is large enough. This means that we may use

percentiles of the Normal distribution, to compute

confidence interval bounds (when

is small, the

is small, the

distribution is often used instead; this is discussed in

statistics texts). In general, a 100(1-

distribution is often used instead; this is discussed in

statistics texts). In general, a 100(1-

)% confidence interval for a single parameter,

)% confidence interval for a single parameter,

say, is computed as

say, is computed as

. Here

. Here

denotes the

denotes the

percentile of the Normal distribution. As previously noted,

percentile of the Normal distribution. As previously noted,

is often chosen to be .05, in which case

is often chosen to be .05, in which case

is approximately 2.

is approximately 2.

As discussed above, one

can reparameterize the model in terms of the new parameter,

and NONMEM will then estimate its standard error. If

re-running the fit presents a problem, there is a simple way

to compute a confidence interval for a function

of a single parameter. If the lower and upper bounds of a

100(1-

of a single parameter. If the lower and upper bounds of a

100(1-

)% confidence interval for

)% confidence interval for

are denoted

are denoted

and

and

, respectively, then a 100(1-

, respectively, then a 100(1-

)% confidence interval for

)% confidence interval for

has lower and upper bounds

has lower and upper bounds

and

and

, respectively. This confidence interval, however, is not

necessarily centered at

, respectively. This confidence interval, however, is not

necessarily centered at

.

.

A truly new feature

introduced by multiple parameters is the phenomenon of

correlation among parameter estimates. NONMEM outputs a

correlation matrix for the parameter estimates. The

element of the matrix is the correlation between the ith and

jth parameter estimates. A large correlation (e.g.

element of the matrix is the correlation between the ith and

jth parameter estimates. A large correlation (e.g.

) means that the conditional distribution of the ith

estimate, given a fixed value of the jth estimate, depends

considerably on this fixed value. Sometimes each parameter

estimate of a pair that is highly correlated has a large

standard error, meaning that neither parameter can be

well-estimated. This problem may be caused by data that do

not distinguish among the parameters very well, while a

simpler model, or a different design, or more data might

permit more precise estimates of each.

) means that the conditional distribution of the ith

estimate, given a fixed value of the jth estimate, depends

considerably on this fixed value. Sometimes each parameter

estimate of a pair that is highly correlated has a large

standard error, meaning that neither parameter can be

well-estimated. This problem may be caused by data that do

not distinguish among the parameters very well, while a

simpler model, or a different design, or more data might

permit more precise estimates of each.

As a simple example,

imagine a straight line fit to just two points, both at the

same value of

: neither slope nor intercept can be estimated at all as

long as the other is unknown, but fixing either one

(simplifying the model) determines the other. Both

parameters could be estimated by observing another point at

some other value of

: neither slope nor intercept can be estimated at all as

long as the other is unknown, but fixing either one

(simplifying the model) determines the other. Both

parameters could be estimated by observing another point at

some other value of

(more data), or, still using just 2 points, by placing these

points at two different values of

(more data), or, still using just 2 points, by placing these

points at two different values of

(modifying the design). Thus, when standard errors are

large, it is useful to examine the correlation matrix of

parameter estimates to see, in particular, if some

simplification of the model may help.

(modifying the design). Thus, when standard errors are

large, it is useful to examine the correlation matrix of

parameter estimates to see, in particular, if some

simplification of the model may help.

There is an approximate

formula for computing a standard error, and hence a

confidence interval for a function of several parameters

(e.g., a confidence interval for half-life when the

estimated parameters are

and

and

). It uses the standard errors of the parameter estimates

and the correlations between the parameter estimates.

However, discussion of this formula is beyond the scope of

this introduction. If a confidence interval for a function

of several parameters is desired, it is often more

convenient to re-fit the data with the model reparameterized

to include the function as an explicit

parameter.

). It uses the standard errors of the parameter estimates

and the correlations between the parameter estimates.

However, discussion of this formula is beyond the scope of

this introduction. If a confidence interval for a function

of several parameters is desired, it is often more

convenient to re-fit the data with the model reparameterized

to include the function as an explicit

parameter.

Before going into details, a note of caution is in order about hypothesis testing in general. The logic of hypothesis testing is that one sets up a hypothesis about a parameter’s value, called the null hypothesis, and asks if the data are sufficiently in conflict with it to call it into question. If they are, one rejects the null hypothesis. However, logically, if they are not, one has simply failed to reject the null hypothesis; one does not necessarily have sufficient data to accept it. An extreme example will make this clear. Let the null hypothesis be any assertion at all about the state of nature. Gather no evidence bearing on the question. Clearly, the evidence (which is void) is insufficient to reject the null hypothesis, but just as clearly, in this case the evidence provides no support for it either.

In less extreme cases there is a way to view failure to reject as lending some support to the null hypothesis, but the matter is problematic. It is somewhat less problematic to use a confidence interval to quantify support for a null hypothesis. A null hypothesis is an assertion that a parameter’s true value is found among a set of null values. A confidence interval puts reasonable bounds on the possible values of a parameter. One can then say that the evidence (the data from which the parameter estimate is derived) does support a null hypothesis (about the value of the parameter) if the null values are included in the interval and that the evidence fully support the null hypothesis if all nonnull values lie outside. An example will help make this clear.

Consider that mean drug clearance in adults varies linearly with the weight of the individual to a clinically significant degree. Formally, this can be put as a statement about a regression coefficient in a model such as

The null hypothesis might

be that

is close to zero, i.e. that it is not so different from zero

as to be clinically significant. To make this precise,

suppose that we know that mean clearance for a 70 kg person

(i.e.,

is close to zero, i.e. that it is not so different from zero

as to be clinically significant. To make this precise,

suppose that we know that mean clearance for a 70 kg person

(i.e.,

) is about 100 ml/min. If

) is about 100 ml/min. If

were .20 ml/min/kg or less, a 50 kg increment (decrement) in

weight from 70 kg would be associated with less than a 10%

change in total clearance. This is clinically insignificant,

so the appropriate null values for

were .20 ml/min/kg or less, a 50 kg increment (decrement) in

weight from 70 kg would be associated with less than a 10%

change in total clearance. This is clinically insignificant,

so the appropriate null values for

might be 0.0 to .20, assuming, of course, that a physical

lower bound for the parameter is zero. (More usually in

statistical discussions a set of null values consists of a

single number, e.g. 0.) If the confidence interval for

might be 0.0 to .20, assuming, of course, that a physical

lower bound for the parameter is zero. (More usually in

statistical discussions a set of null values consists of a

single number, e.g. 0.) If the confidence interval for

only includes null values (e.g., it is .10 to .15), one

might then safely conclude that weight, if it has any effect

at all, has no

only includes null values (e.g., it is .10 to .15), one

might then safely conclude that weight, if it has any effect

at all, has no

significant effect, and that the data fully support the null

hypothesis. If the confidence interval includes null values

and others (e.g., it is 0.0 to .60), one would conclude that

there is some support for the null hypothesis, but that

there is also some support for rejecting it. In this case

the data are insufficient to allow outright acceptance or

rejection. If the confidence interval includes no null

values (e.g., it is .80 to 1.3), one would reject the null

hypothesis and conclude that weight has a clinically

significant (linear) effect on clearance.

significant effect, and that the data fully support the null

hypothesis. If the confidence interval includes null values

and others (e.g., it is 0.0 to .60), one would conclude that

there is some support for the null hypothesis, but that

there is also some support for rejecting it. In this case

the data are insufficient to allow outright acceptance or

rejection. If the confidence interval includes no null

values (e.g., it is .80 to 1.3), one would reject the null

hypothesis and conclude that weight has a clinically

significant (linear) effect on clearance.

For these reasons, we urge caution when performing hypothesis tests and suggest that confidence intervals are often more useful. None the less, the popularity of hypothesis tests requires that they be done, and we now describe two methods for so doing, the first somewhat more approximate and less general than the second, but easier to do.

A straight-forward way to test a null hypothesis about the value of a parameter is to use a confidence interval for this purpose. In other words, if the confidence interval excludes the null values, then the null hypothesis is rejected. As described in Section 4.2.2, such a confidence interval is based on the estimated standard error. This method generalizes to a hypothesis about the values of several parameters simultaneously, but this is beyond the scope of this introduction.

An approach that involves the extra effort of re-fitting the data has the advantage of being less approximate than the one that uses a confidence interval based on the SE. This method is the so-called Likelihood Ratio Test.

The basic idea is to compare directly the goodness of fit (as indicated by the minimum value of the extended least squares objective function) obtained between using a model in which the parameter is fixed to the hypothesized value (the reduced model) and a model in which the parameter must be estimated (the full model).

A model is a reduced model of a full model if it is identical to the full model except that one or more parameters of the latter have been fixed to hypothesized values (usually 0). Consider the examples:

E.g. #1. Valid Full/Reduced Pair:

Full

model:

Reduced

model:

E.g. #2. Invalid Full/Reduced Pair:

Full

model:

Reduced

model:

In example #1, fixing

to 0 produces the reduced model, while in example #2, no

parameter of the full model can be fixed to a particular

value to yield the "reduced" model. It will always

be true that if the models are set up correctly, the number

of parameters that must be estimated will be greater in the

full model than in the reduced model. Note that this is not

so for example #2.

to 0 produces the reduced model, while in example #2, no

parameter of the full model can be fixed to a particular

value to yield the "reduced" model. It will always

be true that if the models are set up correctly, the number

of parameters that must be estimated will be greater in the

full model than in the reduced model. Note that this is not

so for example #2.

The reduced model expresses the null hypothesis; the full model expresses an alternative hypothesis. In example #1 above, the null hypothesis is "typical value of clearance is independent of weight", and the alternative is "typical value of clearance depends linearly on weight."

Note an important point here: the alternative hypothesis represents a particular alternative, and the likelihood ratio test using it will most sensitively reject the null hypothesis only when this particular alternative holds. If the full model were that "the typical value of clearance is inversely proportional to weight" (so that as weight increases, the typical value of clearance decreases, a situation which rarely holds), the likelihood ratio test using the alternative we have stated would not be particularly sensitive to rejecting the null hypothesis, and we might fail to do so. In contrast, we might succeed in rejecting the null hypothesis if we used some other alternative model closer to the truth.

Part of the NONMEM output

is the "Minimum Value of the Objective Function"

(see Chapter 2). Denote this by

. If NONMEM’s approximate model were the true model,

then

. If NONMEM’s approximate model were the true model,

then

would be minus twice the maximum logarithm of the likelihood

of the data (for those readers unfamiliar with likelihoods,

and curious as to what they are, we suggest consulting a

statistics textbook). Statistical theory tells us that the

difference in minus twice the maximum log likelihoods

between a full and reduced model can be referenced to a

known distribution. Thus, to perform the Likelihood Ratio

Test, one proceeds as follows.

would be minus twice the maximum logarithm of the likelihood

of the data (for those readers unfamiliar with likelihoods,

and curious as to what they are, we suggest consulting a

statistics textbook). Statistical theory tells us that the

difference in minus twice the maximum log likelihoods

between a full and reduced model can be referenced to a

known distribution. Thus, to perform the Likelihood Ratio

Test, one proceeds as follows.

Let

be the minimum value of the objective function from the fit

to the full model, and let

be the minimum value of the objective function from the fit

to the full model, and let

be the corresponding quantity from the fit to the reduced

model. Fit both models separately yielding

be the corresponding quantity from the fit to the reduced

model. Fit both models separately yielding

and

and

, and form the statistic,

, and form the statistic,

This statistic is

approximately distributed chi-square (

) with

) with

degree of freedom, where

degree of freedom, where

is the number of parameters whose values are fixed in the

reduced model. For an

is the number of parameters whose values are fixed in the

reduced model. For an

-level test, compare

-level test, compare

to

to

, the 100(1-

, the 100(1-

) percentile of the

) percentile of the

distribution.

distribution.

In particular, when

exactly one parameter of the full model is fixed in the

reduced model, a decrease of 3.84 in the minimum value of

the objective function is significant at

.

.

If NONMEM’s

approximate model (linear in the random effects) were the

true model, and in addition,

were linear in the fixed effects, then

were linear in the fixed effects, then

would be (approximately) distributed according to the

would be (approximately) distributed according to the

distribution with

distribution with

, and

, and

degrees of freedom (

degrees of freedom (

). Since

). Since

is equal to

is equal to

only when

only when

is "large", and is greater otherwise, it is more

conservative to reference

is "large", and is greater otherwise, it is more

conservative to reference

to

to

in all instances, even when

in all instances, even when

is nonlinear.

is nonlinear.

An idea related to

hypothesis testing is this: when faced with alternative

explanations (models) for some data, how does one use the

data to determine which model(s) is (are) most plausible?

When one of the models is a reduced sub-model of the other,

and there is some

reason to prefer the reduced model to the alternative, then

the Likelihood Ratio test can be used to test whether this a

priori preference must be rejected (at the

reason to prefer the reduced model to the alternative, then

the Likelihood Ratio test can be used to test whether this a

priori preference must be rejected (at the

level). However, when one gives the matter some thought,

there is usually little objective reason to prefer

one model over another on a priori grounds. For example,

although possibly more convenient, a monoexponential model

is, if anything, less likely on biological grounds than a

biexponential.

level). However, when one gives the matter some thought,

there is usually little objective reason to prefer

one model over another on a priori grounds. For example,

although possibly more convenient, a monoexponential model

is, if anything, less likely on biological grounds than a

biexponential.

Not only may there not be

a clear

probability favoring one contending model over another, but

the two models may not form a full and reduced model pair.

In such circumstances, one must rely on some goodness-of-fit

criterion to distinguish between the models. Consider

choosing between just two models (the ideas to be discussed

readily generalize to more than two), denoted model

probability favoring one contending model over another, but

the two models may not form a full and reduced model pair.

In such circumstances, one must rely on some goodness-of-fit

criterion to distinguish between the models. Consider

choosing between just two models (the ideas to be discussed

readily generalize to more than two), denoted model

and model

and model

. If the number of free parameters in model

. If the number of free parameters in model

(

(

) is the same as that of

) is the same as that of

(

(

), then here is a reasonable criterion: favor the model with

the better fit. Note that there is no

), then here is a reasonable criterion: favor the model with

the better fit. Note that there is no

value associated with this statement; no hypothesis is being

tested.

value associated with this statement; no hypothesis is being

tested.

Unfortunately, if

one cannot simply compare

one cannot simply compare

and

and

and choose the one with the smaller value. The reason is

best understood when

and choose the one with the smaller value. The reason is

best understood when

and

and

are a full and reduced model pair. The full model will

always fit the data better (i.e., have a smaller

are a full and reduced model pair. The full model will

always fit the data better (i.e., have a smaller

) as it has more free parameters to adjust its shape to the

data. While the same is not always true for any pair of

non-linear models with different numbers of parameters, it

is often true: the model with the greater number of

parameters will fit a given data set better than the model

with fewer parameters. Yet the larger (more parameters)

model may not really be better; it may, in fact, fit an

entirely new data set worse than the simpler model if its

better fit to the original data was simply because it

exploited the flexibility of its extra parameter(s) to

better fit some random aspect of that data.

) as it has more free parameters to adjust its shape to the

data. While the same is not always true for any pair of

non-linear models with different numbers of parameters, it

is often true: the model with the greater number of

parameters will fit a given data set better than the model

with fewer parameters. Yet the larger (more parameters)

model may not really be better; it may, in fact, fit an

entirely new data set worse than the simpler model if its

better fit to the original data was simply because it

exploited the flexibility of its extra parameter(s) to

better fit some random aspect of that data.

Based on the above

intuitive argument, it seems that one should penalize the

larger model in some way before comparing the likelihoods.

This intuition is formally realized in the Akaike

Information Criterion (AIC) which says that one should

compute

+

+

, and choose model

, and choose model

if

if

is >0, and model

is >0, and model

if

if

is <0. The second term penalizes model

is <0. The second term penalizes model

if

if

, and vice versa. When

, and vice versa. When

, the

, the

reduces to the comparison of

reduces to the comparison of

and

and

described previously.

described previously.