Chapter 3 - Models for Individual Data

In this chapter, the notation and definitions we will use to discuss models for individual data will be presented. The relationship of these models to data will be discussed, and a distinction between pharmacokinetic structural models (that describe the underlying shape and form of the data) and statistical error models (that describe the "errors" or differences between observations and structural model predictions) will be made. Several error models will be discussed, as will a useful modelling device, the indicator variable.

By individual data we usually mean data from a single individual (animal or human). One could also be concerned with data comprised of a pharmacokinetic response at just one time point from each of a number of individuals. Call this type of data single- response population data. This name comes from the fact that data such as these can, of course, be regarded as a particular instance of the more general data type, population data; i.e., data comprised of one or more pharmacokinetic responses at different time points from a number of individuals sampled from a population. Although one can discuss the treatment of single-response population data as population data, they are often treated just as are individual data.

A simple pharmacokinetic model for data from a single individual is the monoexponential ("one-compartment") model:

This model describes the

typical time course of amount of drug in the body (

), as a function of initial dose (

), as a function of initial dose (

), time (

), time (

), and a parameter,

), and a parameter,

. As we may be interested in

. As we may be interested in

at several possible times, we explicitly note this by the

subscript

at several possible times, we explicitly note this by the

subscript

which indexes a list of times,

which indexes a list of times,

.

.

A way to write a generic form for a structural model, omitting details of its structure, is

where

stands for some "response" (dependent variable) of

interest (

stands for some "response" (dependent variable) of

interest (

in (3.1)), the symbol

in (3.1)), the symbol

stands for the unspecified form of the model (a

monoexponential such as in (3.1)), which is a function of

known quantities,

stands for the unspecified form of the model (a

monoexponential such as in (3.1)), which is a function of

known quantities,

(

(

and

and

in (3.1)), and parameters,

in (3.1)), and parameters,

(

(

in (3.1)). The quantities in x are known, because

they are either measured or controlled, and therefore, are

called fixed effects, in contrast to effects which

are not known and are regarded as random (see below). The

parameters in the parameter vector

in (3.1)). The quantities in x are known, because

they are either measured or controlled, and therefore, are

called fixed effects, in contrast to effects which

are not known and are regarded as random (see below). The

parameters in the parameter vector

are called fixed effect parameters because they

quantify the influence of the fixed effects on the dependent

variable. Each one of an individual’s pharmacokinetic

parameters is a particular type of fixed effect parameter.

With NONMEM, parameters comprising

are called fixed effect parameters because they

quantify the influence of the fixed effects on the dependent

variable. Each one of an individual’s pharmacokinetic

parameters is a particular type of fixed effect parameter.

With NONMEM, parameters comprising

are (usually) fixed effect parameters, but these may or may

not be an individual’s pharmacokinetic parameters

(contrast figures 2.1 and 2.6). Here we shall use the symbol

are (usually) fixed effect parameters, but these may or may

not be an individual’s pharmacokinetic parameters

(contrast figures 2.1 and 2.6). Here we shall use the symbol

for the parameter vector comprised specifically of an

individual’s pharmacokinetic parameters (although

there will be some exception to this).

for the parameter vector comprised specifically of an

individual’s pharmacokinetic parameters (although

there will be some exception to this).

Aside from the fact that

the values given by a structural model are usually not the

values observed due to measurement error or model

misspecification, an amount of drug (

of (3.1)) is usually not itself observable. Instead, we may

observe a concentration (

of (3.1)) is usually not itself observable. Instead, we may

observe a concentration (

) of drug. We need an "observation scaling" model

to describe the relationship between

) of drug. We need an "observation scaling" model

to describe the relationship between

and

and

. This might be

. This might be

where V is another

parameter, Volume of Distribution. (We denote the

concentration in model (3.3) by the symbol

, to distinguish it, the model-predicted value, from the

actually observed value,

, to distinguish it, the model-predicted value, from the

actually observed value,

. This will soon be discussed further.) PREDPP assumes that

there is always an observation scaling model like (3.3) that

relates an amount of drug (in some compartment of the body)

to the observation, and therefore always expects a

parameter,

. This will soon be discussed further.) PREDPP assumes that

there is always an observation scaling model like (3.3) that

relates an amount of drug (in some compartment of the body)

to the observation, and therefore always expects a

parameter,

that scales (i.e. divides) the predicted amount in the

that scales (i.e. divides) the predicted amount in the

compartment. In the example above,

compartment. In the example above,

is simply

is simply

. In other examples, to be discussed later,

. In other examples, to be discussed later,

can be more complicated. If a value for

can be more complicated. If a value for

is not specified, it is taken to be 1. For the rest of this

discussion, it is convenient to assume that

is not specified, it is taken to be 1. For the rest of this

discussion, it is convenient to assume that

itself includes a scaling parameter (if such is needed, and

even though such a parameter is not usually regarded as one

of an individual’s pharmacokinetic parameters) and

that

itself includes a scaling parameter (if such is needed, and

even though such a parameter is not usually regarded as one

of an individual’s pharmacokinetic parameters) and

that

actually includes observational scaling. Note, considering

the example of (3.3), that

actually includes observational scaling. Note, considering

the example of (3.3), that

, and

, and

. Thus

. Thus

and

and

of (3.1) are in general lists of things (vectors), not

single things (scalars).

of (3.1) are in general lists of things (vectors), not

single things (scalars).

PREDPP implements a

number of pharmacokinetic models, such as the

one-compartment model (3.1), (3.3). These will be discussed

more fully in Chapter 7. There is no need for further

general discussion of kinetic models, as we assume the

readers of this document are familiar with pharmacokinetics.

However, two modelling features deserve further comment,

alternative parameterizations and the special parameter,

.

.

Recall the phenobarbital

example of Chapter 2. For the first run, the input

contained, among other things, some lines of code defining

the variables

and

and

, and then the line

, and then the line

K = CL/V

This line was needed

because PREDPP expects the one-compartment model to be

parameterized using the parameter

, the rate constant of elimination, not clearance and volume

of distribution. However, we chose to estimate typical

population values for

, the rate constant of elimination, not clearance and volume

of distribution. However, we chose to estimate typical

population values for

and

and

, so we had to relate these parameters to THETA and then

relate

, so we had to relate these parameters to THETA and then

relate

to

to

and

and

. This is an example of reparametrization of a model so that

the pharmacokinetic parameters used are those of primary

interest to the modeler. In fact, we may use any

parameterization we wish, so long as we are willing to

include the reparameterization line(s) that translate our

parameters into those expected by PREDPP. (Chapter 7

discusses the parameters PREDPP expects for the various

models it implements.) However, there is a program called

TRANS which automatically does this translation. Different

versions of TRANS exist in the PREDPP Library and correspond

to translations of different parameterizations into that

expected by PREDPP.

. This is an example of reparametrization of a model so that

the pharmacokinetic parameters used are those of primary

interest to the modeler. In fact, we may use any

parameterization we wish, so long as we are willing to

include the reparameterization line(s) that translate our

parameters into those expected by PREDPP. (Chapter 7

discusses the parameters PREDPP expects for the various

models it implements.) However, there is a program called

TRANS which automatically does this translation. Different

versions of TRANS exist in the PREDPP Library and correspond

to translations of different parameterizations into that

expected by PREDPP.

Usually, observations are

concentrations. So, as in model (3.3),

will usually be set identical to

will usually be set identical to

. However,

. However,

is not always simply

is not always simply

. Some examples should clarify this point. (In the

discussion below, we avoid the notation

. Some examples should clarify this point. (In the

discussion below, we avoid the notation

, and use

, and use

, to refer to the scale term for the amount in the

compartment in which concentrations are being

measured.)

, to refer to the scale term for the amount in the

compartment in which concentrations are being

measured.)

This almost trivial case

occurs when one wishes to match the units of predicted

responses to those of the data. For example, suppose

is in milligrams, but concentrations are in ng/ml. If no

scaling is done, the units of

is in milligrams, but concentrations are in ng/ml. If no

scaling is done, the units of

will be kiloliters (i.e.,

will be kiloliters (i.e.,

=1 corresponds to

=1 corresponds to

=1000 liters). To avoid this, one might choose the

model

=1000 liters). To avoid this, one might choose the

model

thereby converting the

units of

into micrograms, and since mcg/L

into micrograms, and since mcg/L

ng/ml, the units of

ng/ml, the units of

become liters. Of course, one could recode one’s data,

dividing all concentrations by 1000 (or multiplying the dose

by 1000) and avoid this, but that may not be

convenient.

become liters. Of course, one could recode one’s data,

dividing all concentrations by 1000 (or multiplying the dose

by 1000) and avoid this, but that may not be

convenient.

Later in this chapter we will discuss a model used when the data arise from two different assays (call them assay 1 and assay 2). In such a case, there may be a systematic (multiplicative) bias of one assay relative to the other. If we wish to allow for this possibility, we might need a model such as

where

is a new parameter that measures the proportional bias of

the assays (i.e., bias causes the apparent volume of

distribution to be different for data from the two assays).

The parameter

is a new parameter that measures the proportional bias of

the assays (i.e., bias causes the apparent volume of

distribution to be different for data from the two assays).

The parameter

is not really a pharmacokinetic parameter, but for the

purpose of this discussion it can be included in

is not really a pharmacokinetic parameter, but for the

purpose of this discussion it can be included in

.

.

Later in this chapter we

will describe a model useful when two kinds of responses are

measured, plasma and urine concentrations. In the case of

urine concentrations, the predicted total drug in the urine

during a time period (available from an "output"

compartment present in all models implemented by PREDPP; see

Chapter 7) would have to be scaled by the actual urine

volume during that time period. This volume would be an

element of

, and

, and

would be set equal to it.

would be set equal to it.

One does not, in fact, ever observe the predicted plasma concentration (or any other predicted response). What one observes is a measured value which differs from the predicted value by some (usually small) amount called a residual error (also called intra-individual error). We regard this error as a random quantity (see below). We will want NONMEM to fit our model to our data, and in so doing, provide us with estimates of the model parameters. The way NONMEM’s fit follows the data is determined largely by what we tell it about the nature of the errors (see Chapter 5). We must therefore provide NONMEM with another model, an error model.

There are many reasons

that the actual observation may not correspond to the

predicted value (e.g.

as given by the right side of (3.3)) The structural model

may only be approximate, or the quantities in

as given by the right side of (3.3)) The structural model

may only be approximate, or the quantities in

may have been measured with error, or, as is always true,

pharmacokinetic responses may be measured with some error

(assay error). It is too difficult to model all these

sources of error separately, so we usually make the

simplifying assumption that each difference between an

observation and its prediction (i.e. each error) is a

randomly occurring number. When the data are from a single

individual, and the error model is the Additive error model

(see Section 3.1, below), the error is denoted by

may have been measured with error, or, as is always true,

pharmacokinetic responses may be measured with some error

(assay error). It is too difficult to model all these

sources of error separately, so we usually make the

simplifying assumption that each difference between an

observation and its prediction (i.e. each error) is a

randomly occurring number. When the data are from a single

individual, and the error model is the Additive error model

(see Section 3.1, below), the error is denoted by

herein, by ETA in NONMEM output, and by ETA or ERR in

NM-TRAN input. (When data are from a population, and the

same error model is used, this error will be denoted

herein, by ETA in NONMEM output, and by ETA or ERR in

NM-TRAN input. (When data are from a population, and the

same error model is used, this error will be denoted

; see Chapter 4.) Therefore a model for the jth observation,

; see Chapter 4.) Therefore a model for the jth observation,

, could be written

, could be written

Implicit in using the

symbol

in this way is the assumption that all residual errors come

from probability distributions with mean zero and the same

(usually unknown) variance. (The error variance is the mean

squared error.) More complicated error models

involving

in this way is the assumption that all residual errors come

from probability distributions with mean zero and the same

(usually unknown) variance. (The error variance is the mean

squared error.) More complicated error models

involving

can be written (see below). A schematic of model (3.4) is

shown for the structural model of (3.1), (3.3) in figure

3.1. Because this model describes the influence of both

fixed effects (

can be written (see below). A schematic of model (3.4) is

shown for the structural model of (3.1), (3.3) in figure

3.1. Because this model describes the influence of both

fixed effects (

) and random effects (

) and random effects (

), it is called a Mixed Effects Model (hence the

name, NONMEM: NONlinear Mixed Effects

Model). Mixed effects models, in general, may have

more than one random effect, and more than one type of

random effect (Chapter 4); (3.4) is only a particularly

simple example.

), it is called a Mixed Effects Model (hence the

name, NONMEM: NONlinear Mixed Effects

Model). Mixed effects models, in general, may have

more than one random effect, and more than one type of

random effect (Chapter 4); (3.4) is only a particularly

simple example.

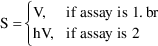

Figure 3.1.

vs

vs

for a monoexponential model. The solid line is

for a monoexponential model. The solid line is

; the circles are the observed data points. An error is

indicated.

; the circles are the observed data points. An error is

indicated.

Even though errors are

unpredictable random quantities, some information about them

is usually assumed, and some can be estimated. First, it is

assumed that the mean error is zero. This simply means that

were the true values for the parameters in

known, the model would have no systematic overall bias

(e.g., be systematically below or above the data points, on

average).

known, the model would have no systematic overall bias

(e.g., be systematically below or above the data points, on

average).

A second aspect of the

error, one that can be estimated by NONMEM, is its typical

size. Since errors may be positive or negative, their

typical size is not given by their mean (which is zero), but

by their standard deviation, the square root of their

variance. One can always simply convert the variance into

the standard deviation, and conversely. NONMEM output gives

estimates of the error variance. With individual data this

variance is denoted in this text by

, and by OMEGA in NONMEM input and output. The standard

deviation (SD) of the error is denoted

, and by OMEGA in NONMEM input and output. The standard

deviation (SD) of the error is denoted

herein. The reason that OMEGA, rather than, for example,

OMEGA SQ stands for

herein. The reason that OMEGA, rather than, for example,

OMEGA SQ stands for

in NONMEM input and output will be discussed in Section 3.8.

(We will see, in Chapter 4, that when the error is

symbolized by

in NONMEM input and output will be discussed in Section 3.8.

(We will see, in Chapter 4, that when the error is

symbolized by

, not

, not

, its variance will be denoted

, its variance will be denoted

in this text, and SIGMA, not OMEGA, in NONMEM input and

output.) Here, the parameter

in this text, and SIGMA, not OMEGA, in NONMEM input and

output.) Here, the parameter

quantifies the influence of the random effect,

quantifies the influence of the random effect,

on the observations,

on the observations,

. It is therefore called a random effects

parameter.

. It is therefore called a random effects

parameter.

The symbol

is always used to denote a random quantity whose probability

distribution has mean zero and variance

is always used to denote a random quantity whose probability

distribution has mean zero and variance

. Model (3.4) says that the errors themselves can be so

regarded, and since an observation equals its prediction

(under the structural model) plus an error, model (3.4) is

called the Additive error model. This model is

illustrated in figure 3.2.

. Model (3.4) says that the errors themselves can be so

regarded, and since an observation equals its prediction

(under the structural model) plus an error, model (3.4) is

called the Additive error model. This model is

illustrated in figure 3.2.

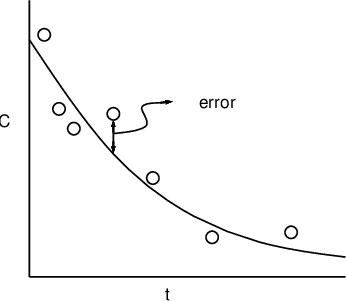

Figure 3.2.

vs

vs

for a monoexponential model. The middle line is

for a monoexponential model. The middle line is

; the outer lines give the approximate "envelope"

for additive errors. Don’t be fooled by the apparent

widening of the gap between the upper and lower curves as

time increases: the vertical distance from the middle line

to either outer line is everywhere the

same.

; the outer lines give the approximate "envelope"

for additive errors. Don’t be fooled by the apparent

widening of the gap between the upper and lower curves as

time increases: the vertical distance from the middle line

to either outer line is everywhere the

same.

NONMEM allows an error model which can be more complicated than that of (3.4). One such more complicated, but useful model is the Constant Coefficient of Variation (CCV), or Proportional error model,

A fractional error is an

error expressed as a fraction of the corresponding

prediction. The CCV model says that a fractional error can

be written as an

, i.e. as a random quantity with mean zero and variance

, i.e. as a random quantity with mean zero and variance

. Under this model, the variance of an error itself is

proportional to the squared prediction, with

. Under this model, the variance of an error itself is

proportional to the squared prediction, with

being the proportionality factor, and so is not constant

over observations. Since, under this model, the standard

deviation of the error, and also of

being the proportionality factor, and so is not constant

over observations. Since, under this model, the standard

deviation of the error, and also of

, is

, is

, and since the mean of

, and since the mean of

is

is

(when

(when

assumes its true value), the coefficient of variation of

assumes its true value), the coefficient of variation of

is just the constant

is just the constant

(the coefficient of variation of a random quantity is

defined as its standard deviation divided by its mean). This

is the reason the CCV error model is so named. Also for this

reason,

(the coefficient of variation of a random quantity is

defined as its standard deviation divided by its mean). This

is the reason the CCV error model is so named. Also for this

reason,

is dimensionless, in contrast to having units equal to those

of the squared observation as with the Additive model. This

error model is illustrated in figure 3.3.

is dimensionless, in contrast to having units equal to those

of the squared observation as with the Additive model. This

error model is illustrated in figure 3.3.

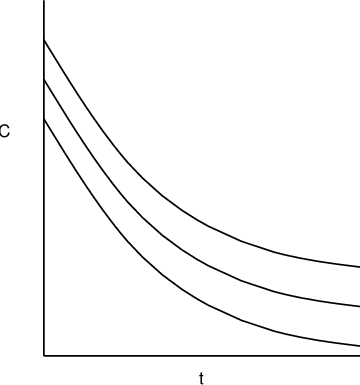

Figure 3.3.

vs

vs

for a monoexponential model. The middle line is

for a monoexponential model. The middle line is

; the outer lines give the approximate "envelope"

for constant coefficient of variation

errors.

; the outer lines give the approximate "envelope"

for constant coefficient of variation

errors.

The exponential error model is

This model is sometimes referred to as the log-normal model, because it it is additive if logs are taken (and because eta sj is assumed to be normally distributed):

See Chapter 8, Section 3.2 for a discussion of this model.

When most observations obey the CCV model but some observations may be near the lower limit of detection of an assay, a model which may be useful is one which is a combination of both the Additive and CCV error models:

Here there are two types

of

’s,

’s,

and

and

. The first has variance

. The first has variance

; the second has a possibly different variance,

; the second has a possibly different variance,

. NONMEM permits several types of

. NONMEM permits several types of

’s. Under this model, the variance of the error

portion of the model is

’s. Under this model, the variance of the error

portion of the model is

. When the prediction is near zero, the variance is

approximately constant, namely

. When the prediction is near zero, the variance is

approximately constant, namely

. This is the smallest variance possible and corresponds,

perhaps, to the limit of assay precision. When the

prediction is considerably greater than zero, the variance

is approximately proportional to the squared

prediction.

. This is the smallest variance possible and corresponds,

perhaps, to the limit of assay precision. When the

prediction is considerably greater than zero, the variance

is approximately proportional to the squared

prediction.

A model that has both the additive and the CCV error models as special cases, and smoothly interpolates between them in other cases is the Power Function model:

Here

is raised to the

is raised to the

power in the error model, rather than the

power in the error model, rather than the

power (Additive error model; note

power (Additive error model; note

for any number,

for any number,

) or the first power (CCV model). The parameter

) or the first power (CCV model). The parameter

is a fixed effects parameter, even though its role in the

overall model is to modify the variance model, not the

structural model. With NONMEM all fixed effect parameters

must be elements of the general parameter vector

is a fixed effects parameter, even though its role in the

overall model is to modify the variance model, not the

structural model. With NONMEM all fixed effect parameters

must be elements of the general parameter vector

. If we want the Power Function Model to interpolate between

the additive and CCV models,

. If we want the Power Function Model to interpolate between

the additive and CCV models,

must be constrained to lie between 0 and 1. NONMEM allows

this (see Chapter 9). While one might be tempted to combine

the Power Function model with the Additive model, much as

the CCV and Additive model were combined above, such a

combination model can lead to identifiability difficulties,

and for this reason such a combination should be

avoided.

must be constrained to lie between 0 and 1. NONMEM allows

this (see Chapter 9). While one might be tempted to combine

the Power Function model with the Additive model, much as

the CCV and Additive model were combined above, such a

combination model can lead to identifiability difficulties,

and for this reason such a combination should be

avoided.

Another more complicated

error model can arise when more than one type of measurement

is made. Suppose, for sake of illustration, that the

observations are drug concentrations, but that they are

measured with two different assays. If one assay may be more

precise than the other, then this is equivalent to saying

that one assay has a smaller

than the other. We would like to be able to take this into

account in the analysis (i.e., not pay as much attention to

the less precise observations), and perhaps (if we have

enough data) estimate the relative precision of the assays

as well. To do this in the notation we have introduced, an

independent variable indicating which observations are

obtained with which assay is needed: we call such an

independent variable an indicator variable.

than the other. We would like to be able to take this into

account in the analysis (i.e., not pay as much attention to

the less precise observations), and perhaps (if we have

enough data) estimate the relative precision of the assays

as well. To do this in the notation we have introduced, an

independent variable indicating which observations are

obtained with which assay is needed: we call such an

independent variable an indicator variable.

Let one of the data items

(an element of

) be labeled

) be labeled

, and let

, and let

take the value 1 if the assay used for

take the value 1 if the assay used for

was of the first type, and the value 0, if it was of the 2nd

type. The variable,

was of the first type, and the value 0, if it was of the 2nd

type. The variable,

is an indicator variable, and it allows us to write an

additive type error model, say, as

is an indicator variable, and it allows us to write an

additive type error model, say, as

Here there are two types

of

’s,

’s,

and

and

. The first applies to the first type of assay, and has

variance

. The first applies to the first type of assay, and has

variance

; the second applies to the second type of assay, and has a

possibly different variance,

; the second applies to the second type of assay, and has a

possibly different variance,

. NONMEM permits several types of

. NONMEM permits several types of

’s. Different types of

’s. Different types of

’s can be correlated, and NONMEM can allow this.

However, this is something we would only need to consider in

the example at hand if the same blood sample were measured

by both assays. We will not emphasize this possibility in

this introductory guide. (This possibility also applies to

random variables describing unexplained interindividual

differences with population data; see Chapter 4)

’s can be correlated, and NONMEM can allow this.

However, this is something we would only need to consider in

the example at hand if the same blood sample were measured

by both assays. We will not emphasize this possibility in

this introductory guide. (This possibility also applies to

random variables describing unexplained interindividual

differences with population data; see Chapter 4)

When the assay is done by

the first method,

will be unity, and (3.8) becomes

will be unity, and (3.8) becomes

so that the variance of

the error is

. When the assay is done by the second method,

. When the assay is done by the second method,

will be zero, and (3.7) becomes

will be zero, and (3.7) becomes

so that the variance of

the error is now

. Both

. Both

and

and

are random effect parameters.

are random effect parameters.

An equivalent form of the model that can be implemented easily is

The same need for

separate scales for different measurements can arise when

more than one type of observation is made. Suppose both

plasma concentrations (

) and urine concentrations (

) and urine concentrations (

) are measured. The structural model for

) are measured. The structural model for

might be (3.1), (3.3). If we assume that urine is collected

between each observation of

might be (3.1), (3.3). If we assume that urine is collected

between each observation of

, then the structural model for

, then the structural model for

, the drug concentration in the urine collected between time

, the drug concentration in the urine collected between time

and time

and time

might be

might be

where

is the fraction of drug excreted unchanged (a parameter),

and

is the fraction of drug excreted unchanged (a parameter),

and

is the urine volume collected between time

is the urine volume collected between time

and

and

(a data item)†.

(a data item)†.

----------

† With all

PREDPP pharmacokinetic models there is an output compartment

for which the total amount of drug leaving the system is

computed automatically. The concentration in the urine is

then obtained by setting the scaling parameter for the

output compartment to

.

.

----------

Assuming again, for sake

of the example, that we want to use an additive type error

model for the observations, the problem is that urine

concentrations can be orders of magnitude larger than plasma

concentrations, so that, while an additive error model might

be appropriate for either type of observation alone, the two

types of observations must have different typical error

magnitudes; i.e., different variances (

’s).

’s).

An indicator variable can

again be used. Let the indicator variable

be unity if the

be unity if the

observation is a

observation is a

, and 0 if it is a

, and 0 if it is a

. We now need to use it for both the structural and error

models, so that:

. We now need to use it for both the structural and error

models, so that:

A little thought shows

that the indicator variable selects the correct prediction (

or

or

) and the correct error term for each observation (

) and the correct error term for each observation (

).

).

An equivalent form of the model that can be implemented easily is

Of course, there could be

three types of assays, or more, and similarly, more than two

types of observations. One usually needs one less indicator

variable than types of things to be distinguished. So, if

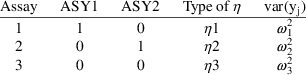

there were three assays, one would define

and

and

.

.

would be 1 if the assay were of the first type, and zero

otherwise;

would be 1 if the assay were of the first type, and zero

otherwise;

would be 1 if the assay were of the second type, and zero

otherwise. The error model for the data would require three

types of

would be 1 if the assay were of the second type, and zero

otherwise. The error model for the data would require three

types of

’s,

’s,

,

,

, and

, and

.

.

Equation (3.11) results in the following:

An equivalent form of the model that can be implemented easily is

We have just seen examples of more complicated error models than the simple Additive model. We here give a mathematical form for the most general mixed effects model that is considered within the scope of this document:

where

is a vector valued function of

is a vector valued function of

and parameters

and parameters

(where the latter is interpreted broadly to contain

parameters such as

(where the latter is interpreted broadly to contain

parameters such as

of (3.7)), and

of (3.7)), and

is a vector of different different

is a vector of different different

types. The notation

types. The notation

denotes vector transpose. When there is more than one

denotes vector transpose. When there is more than one

type, there will be several

type, there will be several

’s, one for each type. The collection of these is

denoted

’s, one for each type. The collection of these is

denoted

and is labeled OMEGA in NONMEM input and output. This

collection is regarded as a diagonal matrix (diagonal for

now; but see Chapter 4), rather than as a vector. We will

use the symbol

and is labeled OMEGA in NONMEM input and output. This

collection is regarded as a diagonal matrix (diagonal for

now; but see Chapter 4), rather than as a vector. We will

use the symbol

and

and

interchangeably in this text to denote the (diagonal)

element of this matrix found in position

interchangeably in this text to denote the (diagonal)

element of this matrix found in position

.

.